Did Trulieve Breach a Covenant?

Disclaimer: This post is for informational purposes only and does not constitute financial advice; readers should conduct their own research and consult a professional advisor before making investment decisions.

On May 7th, pre-market, Trulieve Cannabis Corp. (TRUL on the CSE) reported Q1’2025 earnings. The $1.2 billion Florida-based cannabis company, beat street estimates across the board, with 62% gross margin and cash generation of $51 MM.

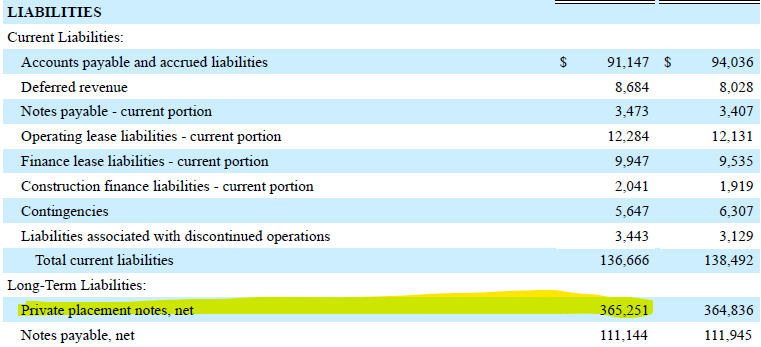

Under the hood, TRUL accumulated a cash balance of $328 MM, a total asset-base of $2.8 Bn and two key liability line items: 1) $365 MM Senior Secured 8% Notes due 2026; and 2) a $500 MM uncertain tax position liability position.

In the fall of 2021, Trulieve issued $350 MM of 5-year Senior Secured 8% bonds. 3 months later the company re-opened the indenture for another $75 MM due to increased demand. The bond was issued as a supplemental indenture to the existing 2019-issued series, albeit with tighter covenants. The bonds are governed by certain incurrence, negative, positive and reporting-based covenants i.e. the company cannot do x, the company must do y, and the company must disclose z. Easy enough to explain.

Here is where things get somewhat complex.

Given Trulieve is a US-based plant-touching cannabis operator, the company must adhere to Federal and State regulation, which places extensive restrictions on the company’s financial operations, specifically it’s ability to bank with, transfer money, pay taxes, and deduct certain expenses under the tax code. We are not here to debate whether these regulations are correct or not, or whether cannabis should be federally illegal, but for now it is.

Within the Federal restrictions is U.S.C Section 280E - Expenditures in Connection with the Illegal Sale of Drugs. Section 280E is one of the most topical and debated regulations within the US cannabis sector today - placing substantially punitive tax impacts on US cannabis operators. The code states:

“No deduction or credit shall be allowed for any amount paid or incurred during the taxable year in carrying on any trade or business if such trade or business (or the activities which comprise such trade or business) consists of trafficking in controlled substances (within the meaning of schedule I and II of the Controlled Substances Act) which is prohibited by Federal law or the law of any State in which such trade or business is conducted.”

To summarize, no expenses can be deducted from the income statement of a US-operating, plant-touching cannabis company due to the illegality of its product/operations, and as such, US cannabis companies are taxed on gross margin. Extremely punitive to free cash flow.

This is the tax code. Plain and clear.

So where is the potential covenant breach? Let’s dive into the indenture.

Article 6 of the Notes Indenture governs the Covenants of the Issuer, Trulieve. So long as the bonds remain outstanding, Trulieve must adhere to the covenants, as described within Article 6.

Section 6.3 of the Covenants of the Issuer describes what the company MUST do with regard to its taxes to remain in good standing with its covenants. The company shall and shall cause each of its restricted subsidiaries to file all tax returns required to be filed and to pay and discharge, or cause to be paid and discharged all taxes shown to be due and payable on such returns.

As of recent, management “adopted a tax position challenging the applicability of 280E to our business last year following the many returns for tax years 2019 through 2021. To date, we have received refund checks totaling over $115 million. Final resolution to our approach may ultimately take years to conclude. In the interim, we continue to accrue an uncertain tax position on our balance sheet while realizing lower cash tax payments.” - Kim Rivers, CEO, Trulieve

The company, through its uncertain tax position build-up, is contesting the IRS’ Section 280E tax liability, and the appropriateness of disallowing certain deductions for businesses dealing with controlled substances (i.e. cannabis), leading to higher taxable income.

Within 6.3 of the Payment of Taxes and Other Claims covenant governed by the indenture, the company can withhold tax payment if two conditions are met:

a) the amount, applicability or validity thereof is contested on a timely basis, in good faith and in appropriate proceedings; and the Issuer or a restricted subsidiary has established an adequate reserve in accordance with IFRS; or

b) the non-payment of all such Taxes in aggregate would not reasonable be expected to have a material effect on the business.

The contested liability is currently on the books for $500 MM. This compares to a $1.2 Bn equity value, or ~40% of the market equity value. I would deem this material to the financial condition of the company, but the covenant is written with an “or”, therefore condition “b)” is satisfied so let’s focus on “a)”.

Under part “a)”, the company has established an “uncertain tax position liabilities” line item on its balance sheet totaling $500 MM. I suspect this is fair value given the materiality of it, and meets the reserve requirement. Trulieve likely satisfies this part of the condition. Moving to the first section of par “a)”, the company is contesting the Section 280E tax in a timely basis, good-faith, and appropriate proceedings. This section needs to be satisfied or there is a potential breach of covenant.

Despite state-level legalization of cannabis in many US states, Section 280E continues to apply because cannabis is considered illegal under Federal law. The litigation Trulieve is bringing forth is with respect to Section 280E - and whether the company must pay tax on gross margin, or whether it should be allowed to deduced expenses in the normal course. This contest seems pretty clear cut.

Here is the nuance to the breach: under the Controlled Substance Act, cannabis remains federally illegal - therefore, the litigation brought forth is not with the IRS or a tax court, rather it is a petition with the Drug Enforcement Agency in Federal courts.

To put a finer point on it, a challenge to cannabis’ Schedule I status is not directly relevant to an IRS audit or tax court proceeding, therefore the IRS lacks jurisdiction to rule on the matter Trulieve is litigating. This means, Trulieve fails to contest Section 280E in an appropriate proceeding, failing to satisfy the Payment of Taxes covenant as it is written. For the contest to be an “appropriate” proceeding under the indenture, it should directly address the validity of the tax liability, rather arguing whether cannabis should be legal is an indirect challenge to Section 280E, one of which the tax courts cannot rule on.

The argument made by Trulieve stretches the indenture’s requirements as it indirectly addresses the validity of the tax code by challenging the underlying law. The result is a $500 MM tax liability - which I view as a call option on federal legislature (whether high probability of success, or not).

Therefore, Trulieve may be in breach of its covenant, 6.3 Payment of Taxes and Other Claims.

If you have any thoughts, shoot me an email at greenshoe.gary@protonmail.com.

Yours truly,

G.G.