Wellington Weekly

Wellington Weekly

Wednesday Market Note (Incl. An ECM Update)

July 21, 2021

Subs -

WE ARE LIVE.

Qualified Canadian Readers Only.

And just like that, volatility is back - just in time for the heights of cottage season to kick in. For live equity issuers, this spells bad news. Pushbacks on valuation / pricing aren’t too uncommon a thing to hear of these days, as exhibited best by Carebook Technologies.

This was originally a C$14M best efforts private placement of common shares that iA Private Wealth launched on June 29 . The deal was slated to close on July 21; except, it hasn’t yet. Yesterday, the original terms of the deal were revised. Now, instead of commons, this healthcare tech company will be offering units (1 sh + ½ wt) in hopes of sweetening the deal.

Not the worst case scenario when the only other option is to bring down valuation. Still, I imagine other issuers won’t be as lucky. I expect more stories to develop in similar fashion over the next few weeks and will be keeping a close eye out for them.

In other news, I would like to divert your attention to something we’ll be seeing a lot more of this month - quarterly banking tear sheets. As the busier half of the year fast approaches, senior bankers around the street will be keen to get these marketing materials in front of as many eyes as possible. This is also perhaps the biggest dick swinging contest on Bay Street internet forums. That being said, let’s go over a few of the contestants.

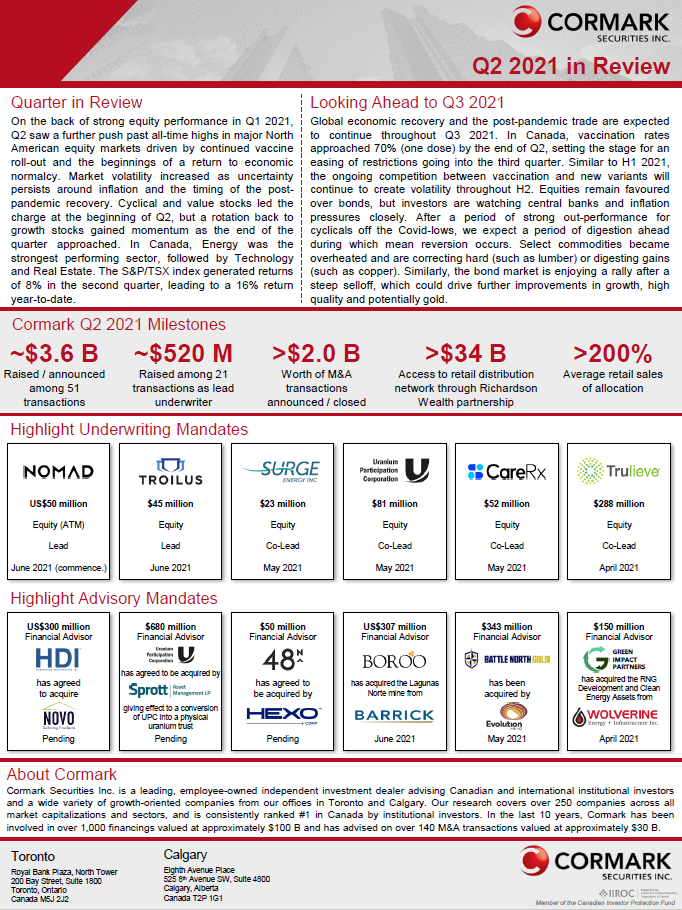

Here we have Cormark’s Q2 2021 in Review. It’s a classic, honest layout. We’ve got some plain vanilla market commentary at the top, with some hard hitting numbers and transactions in the middle. Richardson Wealth also gets a shout out in the middle as Cormark’s retail distribution partner. Big numbers we’re seeing across the date, and unsurprisingly so.

Unsurprisingly, lots of mining transaction highlights here. The subtle addition of Nomad Royalty US$50M ATM speaks to their U.S. distribution and also says “we’re different”, while their work on the 48 North sale to HEXO tells the reader “we know cannabis and are most definitely a Canadian independent”.

Pros:

Classic format, time tested model

Strong coloring, contrast, and dividers / lines

Impressive milestones and transactions

Cons:

Inclusion of pending transactions

Boring tombstone format

Here’s INFOR’s 1H21 Review. Now keep in mind, this is a half year review, so we’ve got numbers from both quarters here. But you can’t deny it - some very impressive credentials. The page is more text heavy, but for good reason. We’ve got direct highlights from and insights into their active advisory and financing franchises. Interesting to note is their mentioning of their podcast (led by ex-GMP Kenrick Sylvestre), Stocks Not Sports, a platform I’ve highlighted a few times before. Impressive milestones across the boards below, and of course, we’ve got the token cannabis advisory deal (Bluma sale to Cresco) tucked in their tombstones.

The coloring of the image at the header, the strong white bordering, the subtle fade into grey, the select serif font, and the citing of Thomson Reuters: this tear sheet says “we’re young, we’re different”.

Pros:

Clean formatting

Recognizable brand name deals

Cons:

1H21 vs. 2Q21

Still not sure how they got to that $40B retail number

If you or your loved ones have access to more tear sheets from other Canadian independents / investment dealers, please send them my way and I will be sure to include them in a separate and archived review post.

ECM World

Top 5 Notable Transactions

Carebook Technologies [Revised @ July 20, 2021]

$14M Best Efforts of Units (1 sh + ½ wt)

Previously common shares

IA w/ CG

Rio2

$25M Marketed SFP of Commons

Scotia w/ CIBC, RJ

Canadian Net REIT

$17.5M Bought of Trust Units

CG w/ Paradigm, CIBC, IA, LB, Desjardins, EWP

Ghost Retail

US$8M Best Efforts of Commons

CG

Spectral Medical

$10M O/N Marketed of Units

Paradigm w/ AGP

Cheers,

G.G.