Wellington Weekly

Wellington Weekly

Wednesday Market Note (Incl An ECM Update)

July 14, 2021

Subs -

WE ARE LIVE.

Qualified Canadian Readers Only.

A busier week this one has been, with Q2 earnings season having all but kicked off. While I don’t imagine that this will pry many hands away from patio tables and cold glasses of drink, rest assured you can count on me staying astutely behind my desk - brows beaten, reporting the good word to you all.

I am - of course - a man of the people.

At last, the long awaited day for retail investors has finally arrived. This morning Flow Beverage Corp. opened the market with its inaugural trading day on the TSX. Founder Nicholas Reichenbach (who also sits on the board of General Assembly Pizza - the infamous pizza subscription service) has awaited this day since he first came up with the idea of boxed water while rolling in the hot desert of Burning Man. Unfortunately, a parched Nicholas didn’t leave his alkaline water idea in Nevada, but brought it back with him to the markets of Canada.

Nicholas and team embarked on a 4-year journey of capital raising for the highly cash burning marketing engine that sold nothing but hopes, dreams, and boxed water, accumulating a rolodex of celebrity endorsements along the way via equity incentive. The company made its rounds across Canada, knocking on retail brokers’ doors - getting quickly turned away given the egregious valuation. Stories have circulated that certain brokers were appalled by Nicholas’ promotional antics, so much so that they walked out of marketing meetings.

Shares were listed at $8.25 on a post-consolidated 5:1 basis, and to no surprise quickly fell to close out the day down 32%, similar to the first trading day of General Assembly. I can only imagine what will happen when locked-up shares come loose.

Notwithstanding my opinion that nothing about this transaction was executed well, Blackrock decided to pick up their cheque-book and lead the company’s latest round - leaning into their ESG mandate. I will highlight two key factors that rub me the wrong way about this transaction:

The first being slightly more palatable. Prior to listing on the TSX, the company performed a share consolidation…the two deadliest words for retail investors in small caps. Naturally, as a small cap equity executes a reverse split and the cap table has funds such as Spartan et al, you best believe the stock will feel the pressure.

Second, and the primary driver as to why I have a bad taste in my mouth. The sheer promotional antics management embarked on over the past 4-years, targeting retail investors who are far less informed when it comes to capitalization tables and promotes…this is where I come in…the green knight. The benefit of broad marketing and mass dissemination of materials is that investors can look back and track how management has progressed, and whether they achieved their stated goals. The downside is accountability. So let’s take a look back and hold the management team accountable:

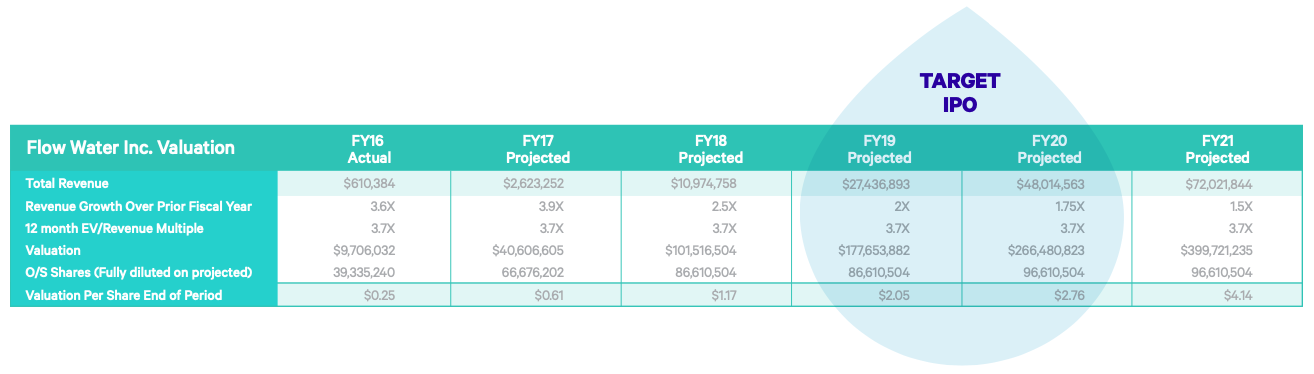

2017

2021E valuation of $4.14 per share

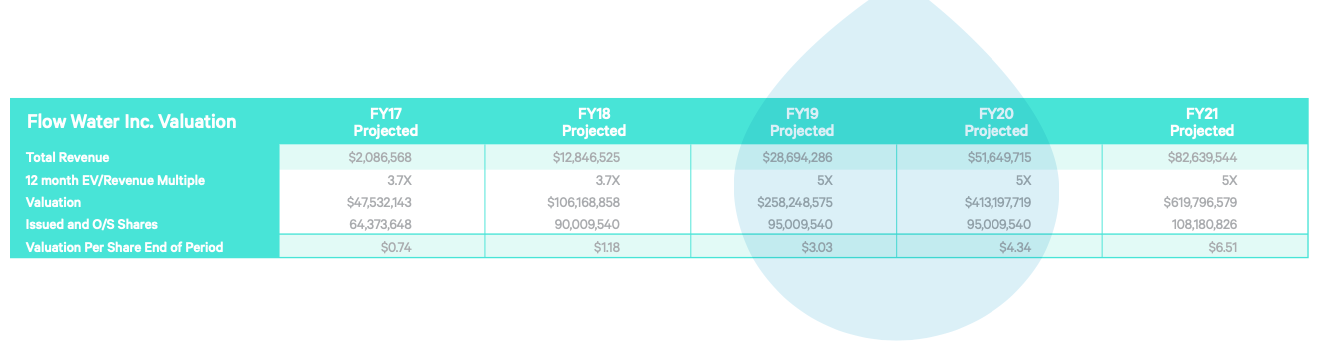

2018

2021E valuation of $6.51 per share

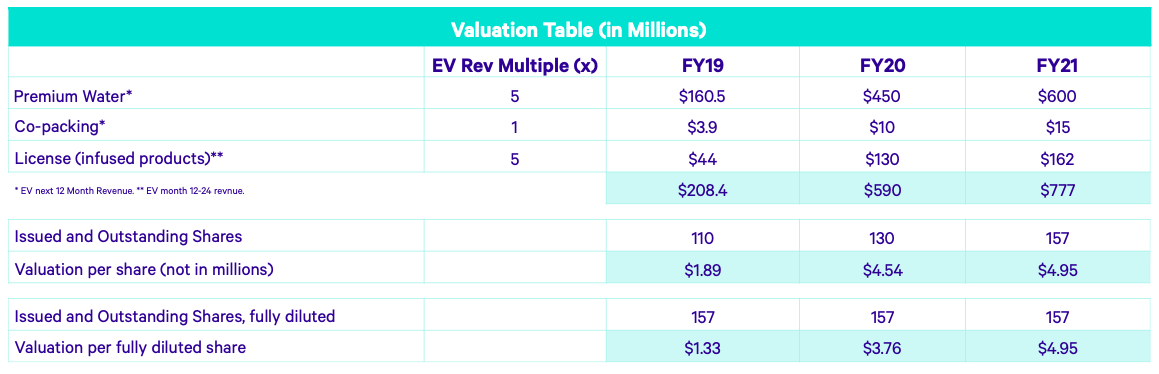

2019

2021E valuation of $4.95 per share

2021 final valuation…$1.65 per share

When raising capital I generally recommend: 1) don’t include pro-forma valuation in your marketing materials to solicit investment; and 2) if you do include pro-forma valuation, include proper disclosures. I’ve reviewed the disclosures included, or lack there of, and as it sits, Flow’s legal team may be in for a busy next couple years - and good to know the folks at Stifel are still up to their GMP antics.

ECM World

Top 3 Notable Transactions

Osisko Green Acquisition (SPAC)

$250M IPO of SPAC Units

8Cap lead

Sabio Mobile

C$10M marketed of Sub Receipts

Beacon w/ Paradigm, PI, EWP

Evergen Infrastructure

$20M IPO of Units (1 sh + 1/2 wt)

DJ w/ Clarius, RBC, EWP, PI, Haywood

Cheers,

GG