Wellington Weekly

Wednesday Market Note (Incl. An ECM Update)

December 4, 2024

Subs -

WE ARE LIVE.

Qualified Canadian Readers Only.

The passing of American thanksgiving and the hangover that follows usually signifies a soft end to the year (and the beginnings of corporate holiday party hopping). Yet in 2024’s final innings, dealers are still itching to secure their top spots on the league tables.

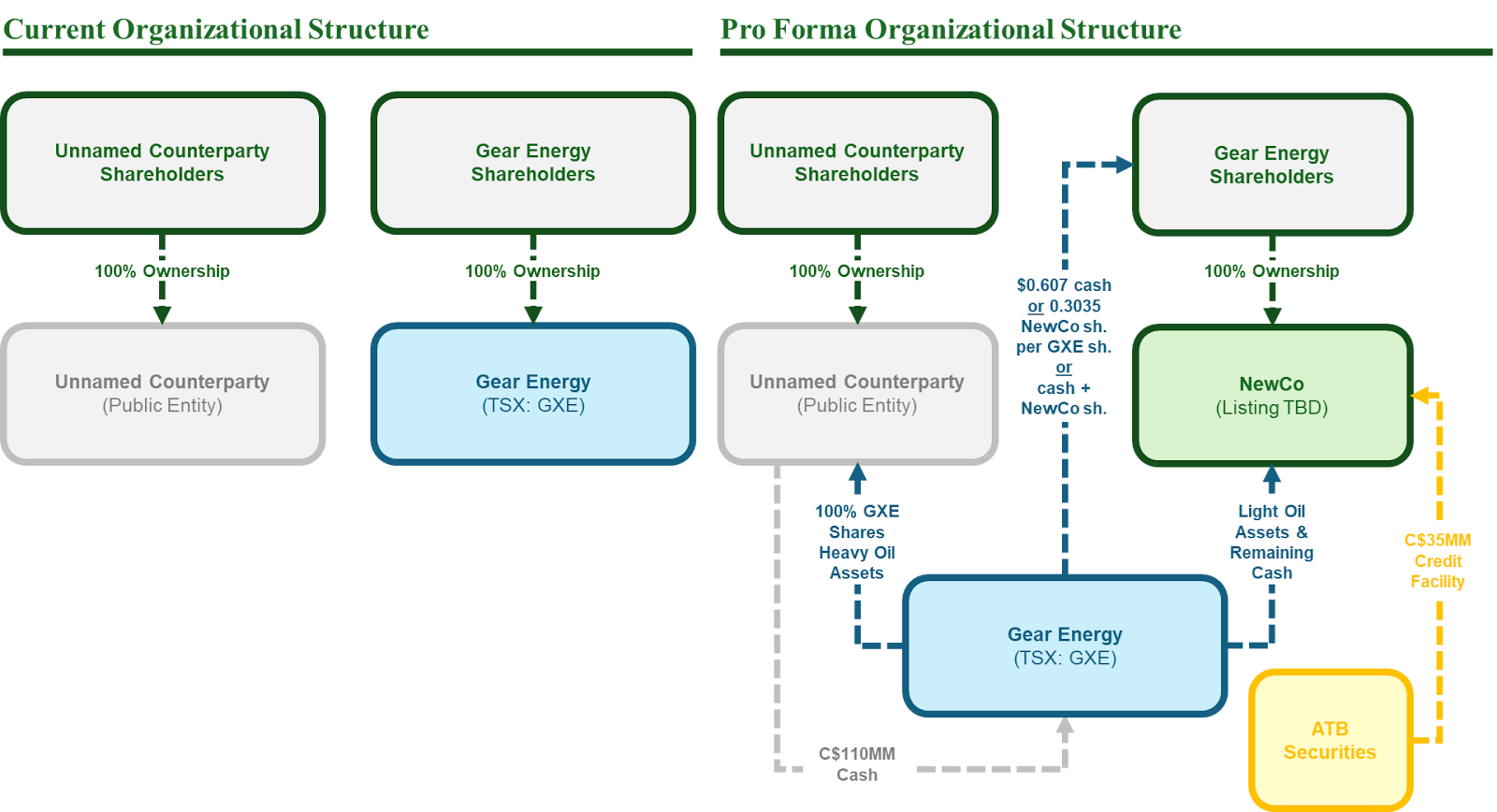

We begin this weekly with a little bit of a case study from the energy complex, where Gear Energy (TSX:GXE) announced a $110MM acquisition and spin-off transaction with an unnamed “large publicly traded company”. Peter’s & Co. (lead) and ATB acted as financial advisors to Gear. For all my non-resource / non-energy readers, don’t click away. I promise this gets interesting.

The transaction contemplates our unnamed counterparty purchasing 100% of the outstanding shares of Gear for $110MM in cash, and Gear transferring its light- and medium-oil Central Alberta, South East Saskatchewan, and Tucker Lake properties into a newly formed spin-off company (“NewCo”).

Gear’s management team and board will run NewCo, and Gear shareholders can elect to receive either (i) $0.607 in cash per Gear sh., (ii) 0.3035 NewCo sh. per Gear sh., or (iii) a yet to be determined combination of cash and NewCo shares. NewCo will be funded by the sum of the remaining cash received from the purchaser and a new $35MM credit facility from ATB.

Below is a visual representation of the transaction:

In short, what we are left with is (i) an effective disposition of Gear’s lower margin, heavy oil assets via the acquisition, and (ii) a complete restart for Gear and its management / board as a newly formed, light-oil focused issuer with a brand new, clean capital structure.

Now, you’re probably asking, “Gary, who’s the unnamed buyer?”, or “Gary, this is overly complicated, why didn’t Gear just conduct an asset sale?”, or perhaps, “Gary, who gives a hoot about a small junior O&G $110MM M&A transaction?” Excellent questions indeed, my friends.

While I have my speculations on who the buyer is, I’d like to focus on answering the last two questions because their answers tie deeply to (i) taxes, (ii) how value tends to be engineered in our country’s oil patch, and (iii) the very identity of Canada’s energy sector.

For starters, a company will not incur (or at the least, greatly minimize) capital gains taxes on spin-offs if it is affected through a share distribution to its existing shareholders. Lower capital gains taxes = more bar money = more Rodenbachs for Gary. That’s pretty simple, easy to follow math. I’ll drink to that.

Secondly, a spin-off is a fantastic opportunity for a company to rebrand, refocus its story and strategic directive, clean out its capital structure, and engineer a re-rating. In Gear’s case, we have a fully-funded NewCo that will be solely focused on liquids weighted, light-oil operations (which in O&G-speak is the most coveted type of oil asset because of its ability to be refined more easily into higher margin end-products) with access to credit from a bank lender. Those qualities have the makings for some great marketing points that I’m sure we’ll hear about in NewCo’s investor materials.

Additionally, management teams will often deliberately undervalue the equity of the spun-off entity as a way of engineering more upside opportunity for themselves and their shareholders. In this situation, pricing and consideration voting results won’t be out for a while, but NewCo is expected to retain 31% of Gear’s total production (or ~1,700 boe/d), making it a much smaller player with potentially more torque.

If I were a serious buyer (and to be clear, I do not own any Gear stock), I’d pay close attention to Gear’s management to see how they take up their transaction consideration. Having a lower valuation at the start also incentivizes management to be more long-term oriented. The more NewCo equity management takes, the better for shareholders.

Lastly, you simply can’t talk about Canada’s energy complex without mentioning spin-offs. Many of the junior / intermediate O&G issuers in Canada that you know and love today are the direct result of these types of deals.

Take Coelacanth Energy (CSE:CEI) for instance, one of Canada’s most successful spin-off stories. This fish-themed energy exploration company was spun off in 2022 as part of Vermilion’s acquisition of Leucrotta (comprising the latter’s mostly undeveloped land sections and assets) at a deemed price of $0.27/sh. On its first day of trading, the company’s shares opened at $0.65/sh. Today, Coelacanth’s equity trades at ~$0.90/sh.

Leucrotta, the company from which Coelacanth was born, was itself a result of an acquisition / spin-off transaction between Long Run Exploration and Crocotta Energy in 2015.

Other Canadian-listed energy names that were born out of spin-offs include: TC Energy / South Bow (ongoing pipeline spin-off), International Petroleum, Topaz Energy, Cenovus, Ovintiv, and Logan Energy.

You simply don’t have a junior / intermediate energy sector in Canada without spin-offs, and this fact is what is so central to the identity of Canada’s energy sector.

Mining assets and issuers come and go through RTOs and promotes; energy assets and issuers come and go through spin-offs and promotes. Of course, you also need the bankers. And right now, the list of dealer competition out in Calgary continues to diminish.

While I was on my ~3 year vacation, the likes of Raymond James and Stifel Canada were shuttering their Calgary offices (sad). The reason? Competing for banking business as an independent-sized firm in the Canadian oil patch has become increasingly more complex.

Broader political and energy transition challenges aside, covering a mid-cap O&G issuer requires comprehensive expertise within the sector and execution capabilities across the entire capital structure (ECM, DCM) and product (M&A, restructuring, derivatives, etc.).

Unfortunately, many independents just aren’t set up this way. The big banks, fully aware of this, have in recent years begun to sweep in and assume some of this smaller-sized coverage (notably NBF, BMO, and Scotia).

And so, as an independent, you are now left with a smaller piece of a pie that was already quite small to begin with. Year to date, the only independent dealers that were truly active as bookrunners in the sector were Echelon (now Ventum), Peters & Co. (an energy-exclusive shop), RCC, and 8Cap.

If you don’t have existing coverage to ride the coattails off of, you are then left to make a difficult choice of either moving your coverage down the value chain or downsizing / stopping all together.

For some dealers, the latter seemed to be the only choice.

On the new issue front, Cormark is looking to make a dent in the league tables before the year ends. At the time of writing, 7 new deals have come to the market since November 27th (all in the mining sector), 2 of which are being led by Cormark.

The largest new issue, from Blue Moon Metals, is a $30MM - $50MM marketed unit deal (1 common share + 9 subscription receipts) in connection with two copper asset acquisitions in Norway. This is a street deal with Cormark as lead left and Scotia as lead right; syndicate includes NBF, Haywood, RJ, and CIBC.

Cormark is also putting up risk capital with CanAlaska Uranium for a ~$10MM bought FT share deal. Cormark is the sole lead, with Desjardins in the syndicate (30%). Books are closed.

Elsewhere, Arizona Metals announced a $25MM bought deal of common shares led by Stifel and Scotia, marking Scotia’s second lead right transaction this week. BMO, NBF, Beacon, and Clarus are in the syndicate. Books are closed.

As an aside, everyone is always glamorizing lead left. Buy why? Seriously. This attitude reminds me of how I viewed the world in my youthful, inexperienced days.

Now, I’ve realized that the real prize in this industry is being lead right. Outsized fee economics for a fraction of the work? Sign me up, every single time. Kudos to Scotia this week for making the difficult, non-status driven choices.

To close the books for 2024, I am also currently working on a yearly equity league table review. In the coming weeks you can expect a special addition of the Wellington Weekly, where I will dive deep into this year’s winners and losers in the Canadian independent broker-dealer scene.

Stay tuned.

ECM World

Top 5 Notable Transactions

Blue Moon Metals

$30MM - $50MM marketed deal of units (1 cs + 9 sr)

Cormark w/ Scotia

Arizona Metals

$25MM bought deal of common shares

Stifel w/ Scotia

Thesis Gold

$10MM marketed deal of common shares

Clarus w/ Cormark

CanAlaska Uranium

$10MM bought deal of FT shares

Cormark

Skyharbour Resources

$6.5MM marketed deal of units (1 FT + 1/2 wt.)

Haywood w/ Red Cloud

With Ease,

G.G.